Become a T+1 expert: Upgrade your settlement workflow now

Ken Finnen is a compliance officer with specific experience in Fixed income and Equity markets. He also specializes in tutoring candidates for a number of FINRA licensing exams, including the Series 7, 9, 10, 24, 63, 65, and 66, as well as the SIE. Ken is the founder of Capital Advantage Tutoring and well-known for his engaging instructional videos and podcast episodes related to FINRA preparation.

Table of contents

- T+1 settlement explained: What FINRA exam candidates need to know

- Key points

- What is T+1 settlement?

- New settlement timing and workflow changes

- What changed with T+1 settlement?

- Risk management and brokerage impact

- But there’s a tradeoff

- Customer experience and compliance adjustments

- Key challenges

- What firms must do

- Trading, dividend tactics, and calculation changes

- Faster access to capital

- Dividend timing is tighter

- Operational impact

- Exceptions, exam pitfalls, and looking ahead to T+0

- Key exceptions

- Looking ahead: T+0 settlement

- T+1 settlement: Series 7 cheat sheet

- Conclusion: T+1 remakes operations and exam strategy

- Next steps for your exam prep

T+1 settlement explained: What FINRA exam candidates need to know

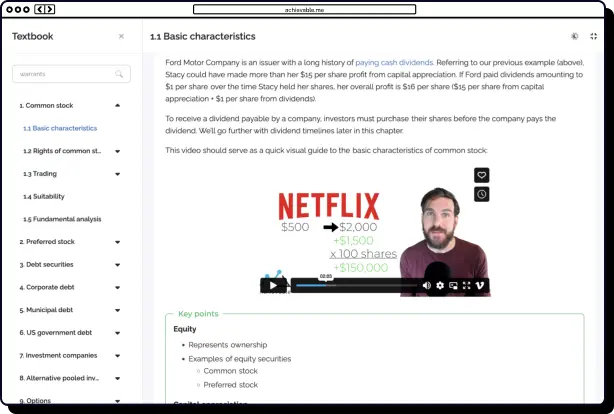

If you’re studying for the Series 7 or another FINRA exam, the shift to T+1 settlement is one of those changes that can quietly trip you up.

It’s not just a definition to memorize. The move from T+2 to T+1 affects dividends, trading timelines, risk management, and even how exam questions are written. Understanding how it works and where candidates commonly make mistakes can give you a real edge.

This guide breaks down what changed, why it matters, and how to apply it on your exam and in real-world scenarios.

Key points

- T+1 settlement shortens trade settlement from two days to one

- The traditional DERP timeline is now outdated

- Faster settlement reduces risk but leaves less room for error

- Not all securities settle on T+1: know the exceptions

- Exam questions increasingly reflect these updated timelines

What is T+1 settlement?

T+1 settlement means that a trade settles one business day after the trade date.

Example:

If you buy a stock on Monday, it settles on Tuesday, not Wednesday, as it did under T+2.

This change impacts how quickly ownership transfers, when funds are available, and how firms manage operations.

New settlement timing and workflow changes

The shift from T+2 to T+1 has fundamentally changed how market operations work.

Previously, the DERP timeline (Declaration, Ex-dividend, Record, Payable dates) aligned with a two-day settlement cycle. Under T+1, that framework no longer holds up.

What changed with T+1 settlement?

- Trades now settle the next business day

- The gap between ex-dividend and record dates has narrowed

- Older dividend timelines can lead to errors if used today

Because of this, firms must:

- Update internal procedures and systems

- Revise training and study materials

- Ensure automated processes reflect the new timeline

Failing to adapt can result in:

- Misallocated dividends

- Settlement failures

- Incorrect client communications

For exam candidates, this is a key takeaway: don’t rely on outdated DERP assumptions.

Risk management and brokerage impact

One of the biggest reasons for the shift to T+1 is risk reduction.

With fewer unsettled trades:

- Credit risk decreases

- Systemic risk is reduced

- Firms are less exposed to market volatility

Under T+2, price swings over two days could disrupt settlement. T+1 cuts that exposure in half.

But there’s a tradeoff

Faster settlement means:

- Less time to fix errors

- Tighter operational deadlines

- Greater need for automation and monitoring

Brokerages must now rely on:

- Real-time systems

- Faster reconciliation processes

- Stronger liquidity management

For your exam, remember: T+1 improves safety but increases operational pressure.

Customer experience and compliance adjustments

Faster settlement doesn’t just affect firms; it also changes client expectations. Customers who once expected delays now anticipate “real-time” completion. The Federal Reserve’s 2023 Payments Study found that over 20% of consumers want immediate access to funds.

Today’s investors increasingly expect near-instant results. T+1 moves in that direction, but it also introduces new risks.

Key challenges

- Clients must fund trades more quickly

- Missed deadlines can lead to failed transactions

- There is less tolerance for errors

Many investors still misunderstand settlement timing, which can lead to confusion.

What firms must do

- Improve communication with clients

- Update compliance monitoring systems

- Catch issues (like insufficient funds) faster

Exam tip: Questions may test your understanding of how timing impacts compliance and client interactions, not just settlement definitions.

Trading, dividend tactics, and calculation changes

T+1 settlement also affects trading strategies and dividend planning.

Faster access to capital

Active traders benefit because:

- Funds become available sooner

- Reinvestment can happen more quickly

Dividend timing is tighter

Strategies like dividend capture now require more precision.

Example:

Under T+1, there’s less time between the trade date and record date, making timing errors more likely.

Operational impact

- Recordkeeping becomes simpler

- Cost basis tracking is clearer

- But outdated systems can cause serious errors

For exams, expect questions that test:

- Timing accuracy

- Dividend eligibility

- Settlement-related calculations

Exceptions, exam pitfalls, and looking ahead to T+0

Not all securities follow T+1 settlement, and this is a common exam trap.

Key exceptions

Some products may still settle on T+2 or T+3, including:

- Certain mutual fund transactions

- Limited partnerships

- Some government or mortgage-backed securities

- Foreign securities

Exam trap example:

A question may imply all securities settle T+1, but the correct answer depends on recognizing exceptions.

Looking ahead: T+0 settlement

The industry is already exploring same-day (T+0) settlement, driven by:

- Real-time payments

- Distributed ledger technology

While faster, T+0 would require:

- Instant error detection

- Even tighter operational controls

T+1 settlement: Series 7 cheat sheet

- Settlement cycle: T+1 (trade date + 1 business day)

- Old rule: T+2 (now outdated)

- DERP timeline: no longer reliable

- Main benefit: reduced risk and faster capital use

- Main challenge: less time to fix errors

- Common mistake: assuming all securities follow T+1

Conclusion: T+1 remakes operations and exam strategy

The move to T+1 settlement is more than a technical update: it reshapes how markets operate.

From dividend timing to risk management and compliance, nearly every aspect of the settlement process has changed. For exam candidates, this means updating your mental models and avoiding outdated assumptions.

Those who understand both how T+1 works and where exceptions apply will be better prepared for tricky, scenario-based questions on the Series 7.

Next steps for your exam prep

- Review updated study materials carefully

- Practice questions involving settlement timing

- Focus on exceptions and edge cases

- Revisit dividend and trading scenarios under T+1

Staying current isn’t optional: it’s required for both passing your exam and succeeding in the industry.